Prices & InflationTrade & International

What interest rates tell you about the oil shock

Since the Strait of Hormuz closed at the end of February, WTI crude oil has risen from $63 to $105 a barrel. Interest rates across the economy have responded. The bond market is pricing the oil shock as temporary. But the uncertainty it introduced has a longer-term cost.

A temporary shock with a long tail

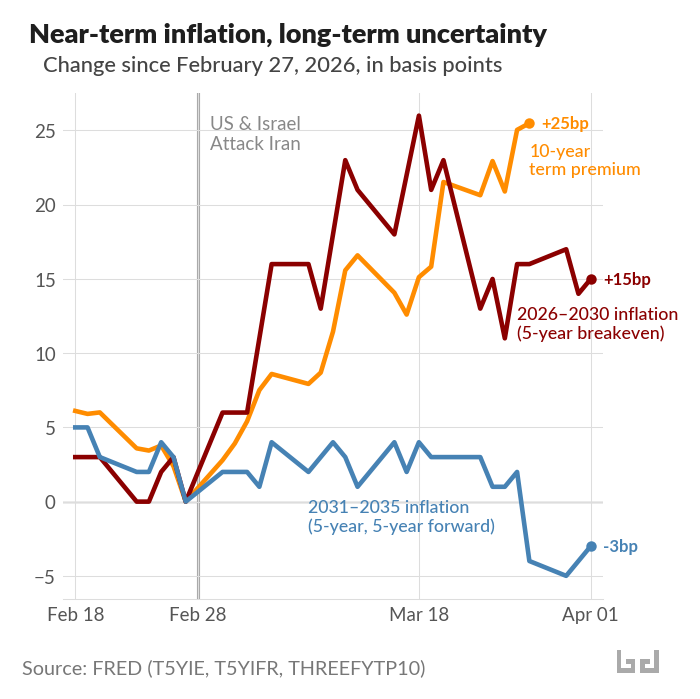

You can read market expectations for future inflation directly from Treasury bonds. The “breakeven” inflation rate is the difference between a regular Treasury yield and the yield on a Treasury Inflation-Protected Security (TIPS) of the same maturity. It tells you the inflation rate the market is betting on.

Since February 27, the five-year breakeven has risen 15 basis points (hundredths of a percentage point) to 2.55%. The market expects somewhat higher inflation over the next five years, which makes sense given an oil price that nearly doubled. But the five-year, five-year forward rate — a measure of expected inflation in years five through ten — actually fell 3 basis points to 2.07%.

In short: near-term inflation expectations rise; long-term expectations stay anchored. Oil futures tell the same story. The August WTI contract is trading around $79, well below the $105 spot price, meaning the market expects the disruption to fade. That said, the IEA has noted that more than 40 energy sites across nine countries have sustained severe damage, which could extend the disruption beyond what futures currently price.

The cost shows up in the term premium

If markets view the inflation shock as temporary, why have longer-term yields risen? The 10-year Treasury yield is up 33 basis points since February 27. Almost all of that increase, 28 basis points, comes from higher real yields. Inflation expectations barely moved.

The explanation lies in the term premium. When investors buy a 10-year bond, they are locking up their money for a decade. The term premium is the extra compensation they demand for taking on that uncertainty: the risk that the economy, inflation, or policy could go in unexpected directions. The Federal Reserve publishes an estimate using a model called Kim-Wright.

Since the war began, the Kim-Wright 10-year term premium has risen 25 basis points. That accounts for most of the rise in the 10-year yield. Investors are pricing in a more uncertain world. Oil supply disruptions and geopolitical conflict make long-term bonds riskier to hold.

The yield curve steepened

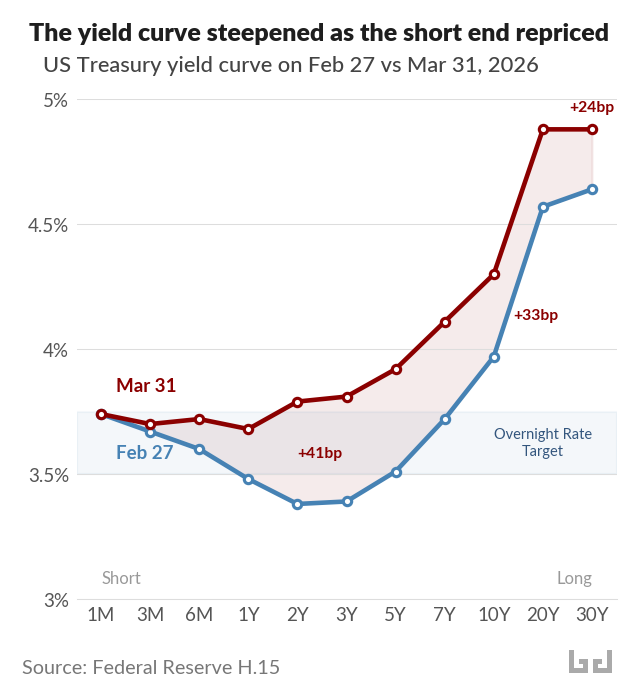

The yield curve plots Treasury yields from the shortest maturities to the longest. Since February 27, it shifted upward across the board, but not evenly. The two-year yield jumped 41 basis points, exceeding the Fed’s overnight rate target of 3.50-3.75%. The 10-year rose 33. The 30-year rose 24.

The short end of the curve reflects expectations about what the Fed will do in the near term. When the two-year yield rises above the overnight rate, it means markets expect the Fed to hold rates where they are. Before the oil shock, core PCE inflation — which strips out food and energy — had already climbed to 3.1% in January, stalling the disinflationary trend from 2023–2024. The oil shock eliminated any remaining room the Fed had to cut.

The real rate dip

The Fed is holding rates steady, but monetary conditions are loosening anyway. As headline inflation rises from the oil shock, the real fed funds rate — the policy rate minus inflation — falls without the Fed doing anything. It has already dropped from about 1.0% in February to 0.4% in March. The OECD forecasts US inflation reaching 4.2% this year; if that materializes with the overnight rate unchanged, the real rate would be roughly -0.5%.

This automatic loosening provides a modest cushion on the demand side during the supply shock. But it only works if the Fed holds steady. Raising rates to chase headline inflation would eliminate the cushion and tighten into a supply disruption. This is a shock that monetary policy cannot fix. The supply problem can only be resolved by reopening the Strait of Hormuz or reducing dependence on oil that passes through it.