Labor MarketMacroeconomics

Labor Market Conditions and Impulse

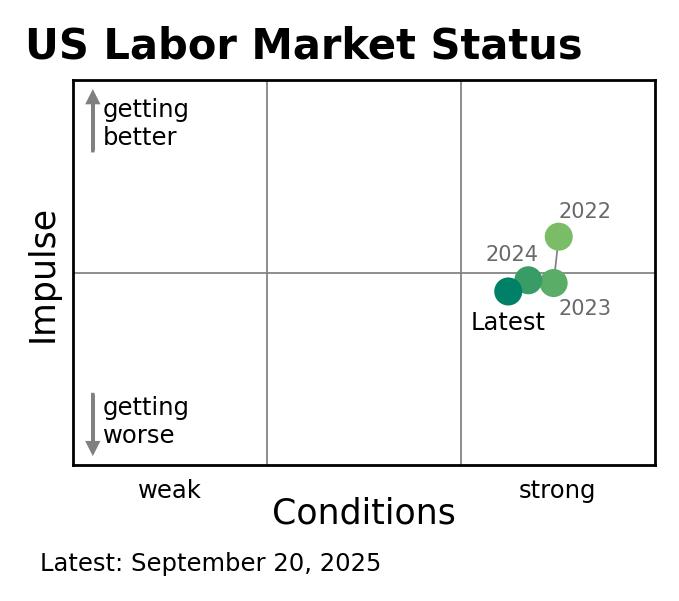

Labor markets can deteriorate very rapidly, resulting in an economic recession. As such, economists monitor conditions closely. Currently, the US labor market is reasonably strong, though conditions have worsened over the past few years. The impulse of the labor market, based on recent changes, suggests further weakening. The Federal Reserve should tread cautiously.

Labor market conditions–our collective ability to find work and bargain for income–are cyclical. Sometimes labor markets are strong and sometimes they are weak. Once conditions start deteriorating, the economy is in trouble, as the process snowballs. Every rapid deterioration in US labor market conditions has coincided with a recession.

To see where we are in the cycle, I combine data on unemployment, employment, job openings, and hiring. Labor market conditions are “strong” when unemployment is low, employment is high, jobs are available, and firms are hiring. A strong labor market is consistent with the Fed full-employment mandate. As of September 20, 2025, conditions are fairly strong, with some deterioration over the past few years.

Additionally, the “impulse” of the labor market is measured by recent changes. Specifically, three-month changes in unemployment, employment, job openings, and hiring are combined with new claims for unemployment insurance. The impulse of the labor market shows conditions slowly getting worse. The pace of deterioration has recently picked up, slightly.

When the labor market impulse turns strongly negative, a recession is likely. Recessions bring immense hardship. Given this dynamic, the Fed should tread cautiously on the labor market.

Instead, the Fed should ramp up the tactic of publicly discussing asset price valuations. If US asset prices are justified by fundamentals, they should hold up well to scrutiny. If, on the other hand, stocks are overvalued, the Fed would be prudent to warn investors. Further, Fed scrutiny of asset prices could cool inflation by tempering wealth effects on consumption.