PolicyWages & Income

Who pays for raising the retirement age

Social Security’s cost is projected to rise from 5.3% of GDP today to about 6% by 2055, according to the 2025 Trustees Report. That is less than one percentage point over 30 years. It is not a crisis. It is a slow, predictable increase in a program that keeps millions of retirees out of poverty.

One of the most common proposals for closing this gap is raising the retirement age. This is not really about when people retire. Raising the full retirement age from 67 to 70 would cut monthly benefits by about 23%, no matter when you claim. It is a benefit cut dressed up as a scheduling change.

Social Security does not need benefit cuts. But the case for raising the retirement age fails on its own terms too. It assumes the people who depend on Social Security can just work longer. They cannot.

Who absorbs that cut?

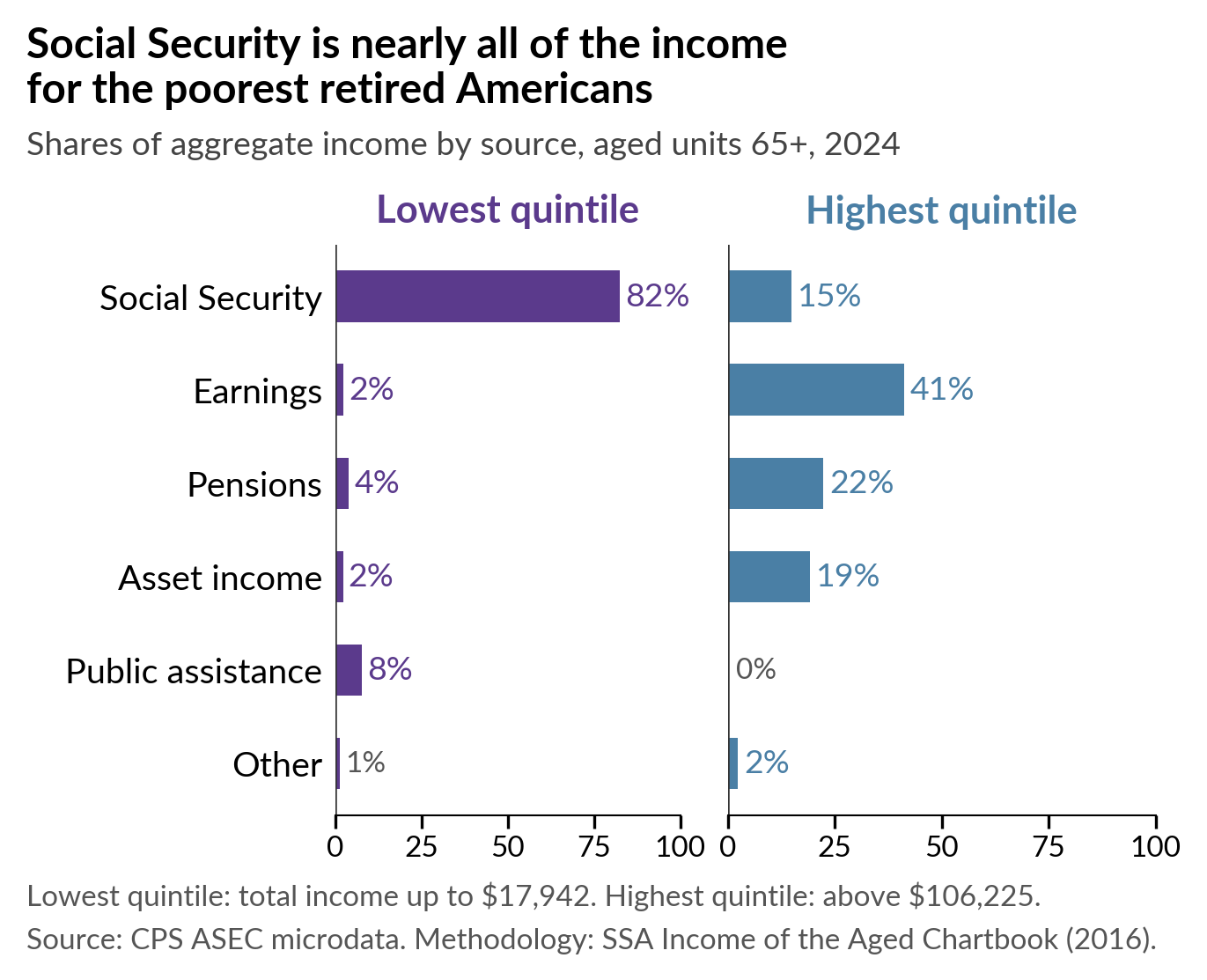

For the poorest retirees, Social Security is nearly everything — 82% of income. Earnings, pensions, and asset income together account for just 8%. For the highest-income retirees, the picture is reversed: earnings make up 41%, pensions and asset income another 41%, and Social Security just 15%. This pattern is clear in the SSA’s Income of the Aged Chartbook, and the chart below shows it holds with 2024 data.

The workers who depend most on Social Security in retirement are the same workers who had the hardest jobs while they were working. And those jobs do not get easier with age.

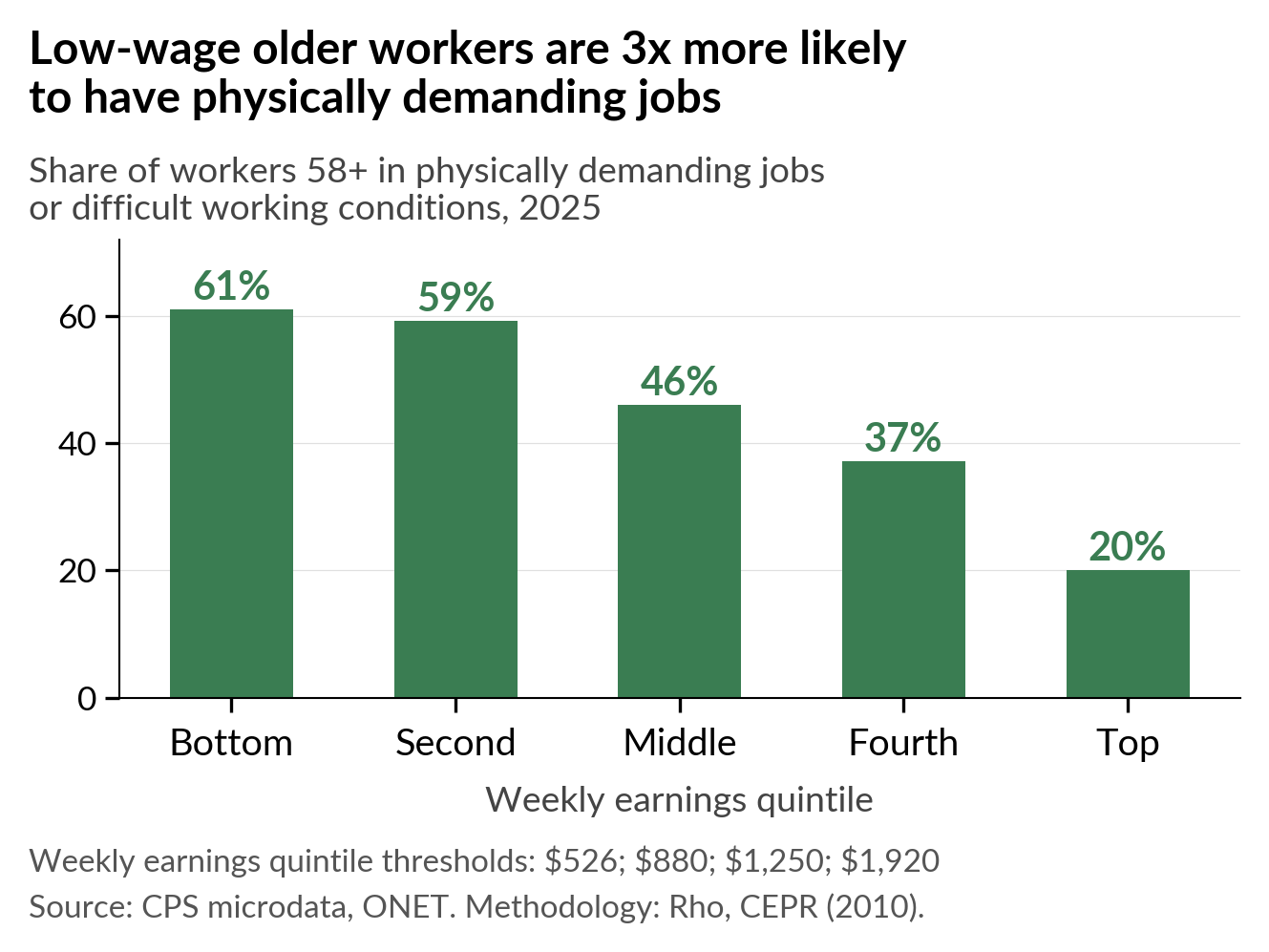

In 2025, the lowest-paid older workers are three times as likely to have physically demanding jobs or difficult working conditions as the highest-paid. In the bottom fifth by wages, 61% of workers 58 and older are in these jobs. That is six in ten. In the top fifth, it is 20%. The most common occupations for these workers are janitors, personal care aides, cashiers, truck drivers, and maids.

These are not jobs you can do forever. The physical toll accumulates, and for many workers the question is not when to retire but whether they will be healthy enough to make it there. Life expectancy at birth for Black men is 70.3 years. Many will pay into Social Security for decades and never collect a check. Raising the retirement age to 70 increases the share of workers who pay in and get nothing back.

Meanwhile, the highest-paid workers — the ones who could most easily extend their careers — are the ones who least depend on Social Security. They have pensions, investment income, and jobs they can do from a chair.

To put the predicted increase in Social Security costs into context, corporate profits after tax have risen from about 6% of GDP in the 1990s to nearly 12% today. That’s about eight times what is needed over the next 30 years to close Social Security’s shortfall. The people who receive corporate profits always seem to find room for more. And most people don’t treat the increase in corporate profits like a crisis.

Raising the retirement age to close a gap of less than one percentage point of GDP means cutting benefits for janitors and home health aides, the people who can least afford to absorb austerity. That is not fiscal responsibility. It is choosing cruelty.