Trade & International

The last energy crisis cost Europe $1.8 trillion. The next one just started.

With the war on Iran disrupting global LNG supply and European gas prices surging, a new energy crisis is taking shape before Europe has recovered from the last one.

A new report by Kevin Cashman for the Transition Security Project, “Trillion Dollar Bills: The Costs of Transatlantic Dependence for Europe,” draws a line that is rarely drawn clearly: from geopolitical decisions, to household costs, to corporate windfalls. Cashman argues that the US pursues “energy dominance” as an explicit foreign policy tool, Europe absorbs the price shocks, and US energy companies collect the difference.

The report puts numbers on each link in that chain. The direct cost of the 2022 energy shock to the EU and UK was roughly €1.7 trillion ($1.8 trillion) from 2022 to 2025 — about two percent of GDP — in higher bills and fiscal support to cushion them. Meanwhile, US oil and gas companies accrued $241 billion in windfall profits in 2022 alone, dwarfing the $36 billion for companies in the European common market and $23 billion in the UK.

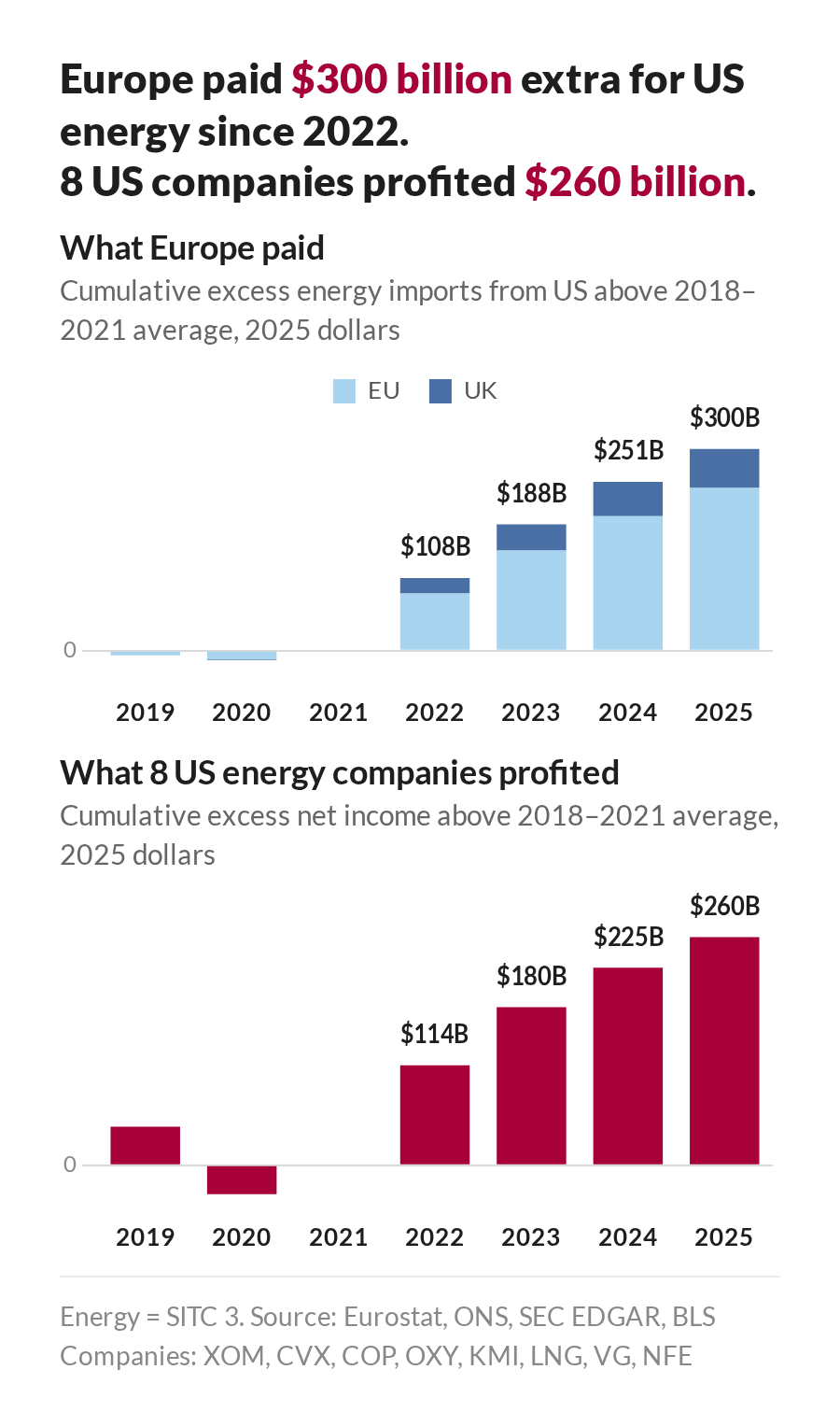

I wanted to zoom in on the bilateral relationship. Using Eurostat, ONS, and SEC filings, I tracked how much the EU and UK paid for energy imports from the US above pre-crisis levels, alongside how much eight major US energy companies profited above those same levels. The companies operate globally, not just in Europe, so these are not mirror images of each other — but the scale and timing tells the story.

From 2022 through 2025, Europe paid an estimated $300 billion more for US energy imports than it would have at pre-crisis rates, adjusted for inflation. Over the same period, the eight US companies collected $260 billion in cumulative excess net income. Semieniuk et al. (2025) map the broader US fossil fuel shareholding network — over 200 companies — and find roughly 250,000 stakeholders, with half of all profits flowing to the wealthiest one percent. As a rough exercise: if you divide the $260 billion from just these eight companies by those 250,000 stakeholders, it comes to about $1 million each.

The underlying problem, as Cashman argues, is that Europe used the last crisis to swap one dependency for another. At the start of 2019, the US supplied about four percent of EU and UK gas imports from outside the European Economic Area. Today, US LNG is roughly 40 percent. Europe did not build energy independence. It changed suppliers. And now, with that supply chain again threatened and Europe’s Russian gas ban taking effect, the same chain — geopolitical shock, household costs, corporate windfall — is already in motion.