Labor MarketMacroeconomics

Employment Is Falling. Is GDP Next?

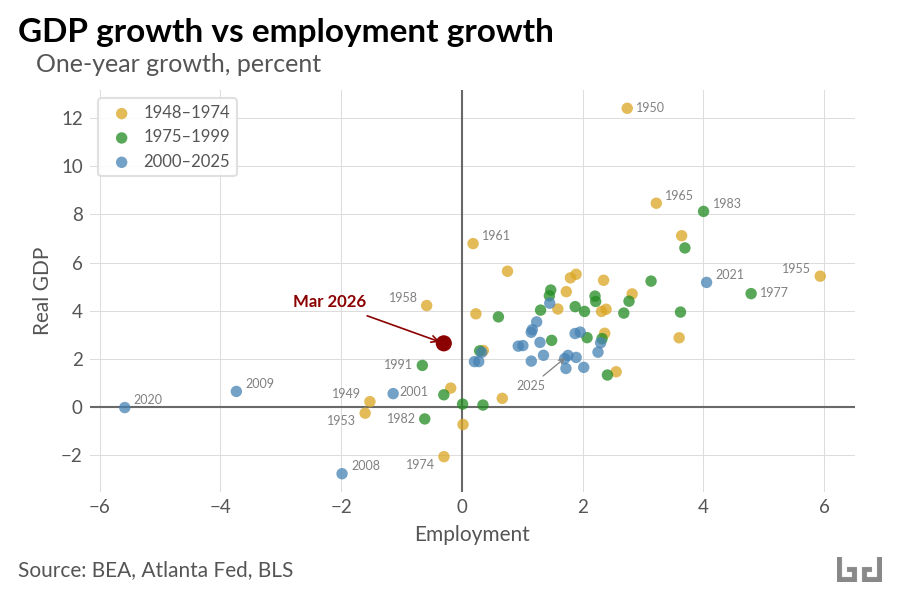

GDP growth and employment growth usually move together. The scatter below plots one-year changes in each, from 1949 to 2025, plus March 2026 in red. The correlation is 0.70.

March 2026 sits in an unusual position: GDP has grown over the past year while employment fell 0.3 percent. That combination shows up a few other times in the data (1958, 1991, 2001, 2009) but in each case the economy was recovering from a recession. There is no recession to recover from in 2026.

A recent FEDS Note by Seth Murray and Ivan Vidangos traces the mechanism. An aging population combined with collapsing net immigration has pushed labor force growth to near zero. The breakeven pace of employment growth has fallen below 10,000 per month, far below any point in the past 65 years. Additionally, federal civilian employment is down 11 percent year-over-year, the steepest peacetime decline on record.

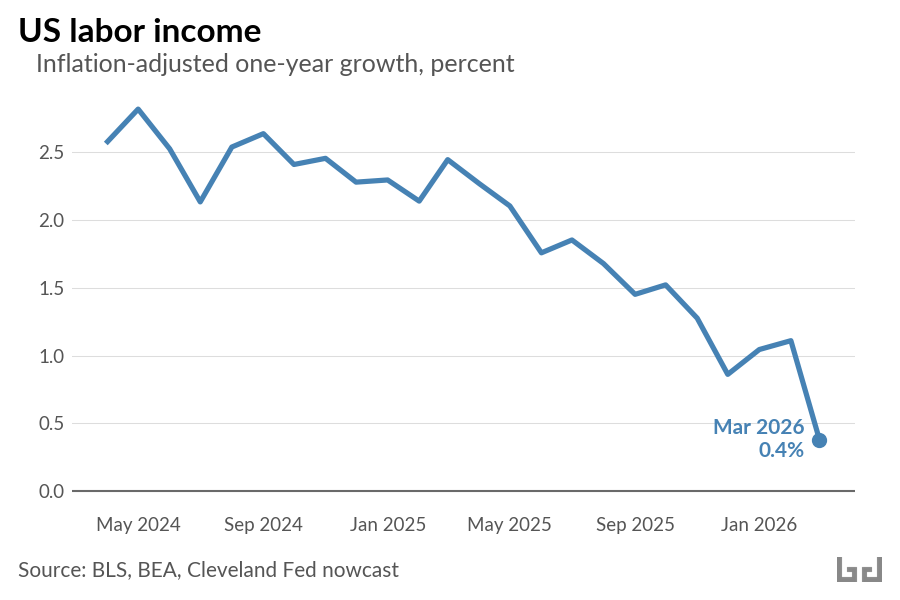

The income side of the economy reflects the job market slowdown. In a healthy economy, US labor income should grow by five percent or more per year. This includes higher wages tied to productivity, cost of living adjustments tied to inflation, and new wages paid to new workers as the workforce grows. Over the past year, amidst a shrinking workforce, nominal gross labor income grew only 3.7 percent. Critically, inflation is now heading toward 3 to 4 percent. The difference between the two measures, real labor income growth, is approaching zero.

GDP growth is decelerating too. After strong quarters in mid-2025 (3.8 and 4.4 percent annualized), Q4 came in at 0.7 percent and the Atlanta Fed Q1 nowcast sits at 1.3 percent. Over the past two quarters, annualized growth averages 1 percent. Coincidentally, Josh Bivens at EPI estimates that about 1 percentage point of recent GDP growth comes from AI-related channels (a stock market wealth effect and capital expenditure) that he characterizes as fragile.

The labor side of the growth equation is stalling. Productivity has to carry everything. That is a lot to ask.